This Tech Stock Has Delivered Palantir-Like Gains. Should You Buy It Now?

Amit Singh

Barchart

1 hour ago

When most investors think of 2025’s biggest winners, Palantir (PLTR) is the first name that comes to mind. The stock has dominated headlines, driven by surging demand for its Artificial Intelligence (Platform) and accelerating revenue growth. Palantir has climbed an impressive 122.7% so far this year, making it one of the top-performing stocks in the S&P 500 Index ($SPX).

But while Palantir has captured all the attention, another tech name has quietly outperformed it. Seagate Technology (STX), best known for its data storage solutions, has risen 147.11% year-to-date, edging out Palantir’s gains. The stock has also been benefiting from AI-driven tailwinds.

What makes Seagate more compelling is that despite its remarkable rally, STX stock still looks appealing from a valuation standpoint, leaving room for additional upside. Let’s take a closer look.

AI Demand and Improving Profitability to Push STX Stock Higher

Seagate is one of the key beneficiaries of the AI boom. As the leading cloud providers and enterprise customers race to expand their infrastructure for AI-driven applications, the company’s mass-capacity storage products are seeing surging demand. Data centers, which serve as the backbone of AI workloads, are scaling up at an unprecedented pace, supporting demand for Seagate’s storage technology.

The strong demand backdrop has translated into impressive financial performance. Seagate closed its fiscal 2025 with revenue up 39% year-over-year, while operating income more than tripled. The leverage from higher sales, and its focus on supply-demand management, cost controls, and a transition to a build-to-order manufacturing model with dynamic pricing, have all contributed to expanding margins.

Looking ahead, Seagate is ramping up production of its next-generation products. Among those products is the heat-assisted magnetic recording (HAMR) hard drive, which began high-volume production in fiscal 2025. These drives are cost- and energy-efficient, which will support future demand.

The momentum is already visible with three major cloud providers having qualified Seagate’s HAMR-based drives, and more customers are in the process of doing so. Alongside this, nearline sales in the enterprise OEM market are recording modest gains, giving management confidence that strong demand will continue in the coming months.

Seagate is likely to deliver strong revenue in fiscal 2026. Moreover, by shifting to a build-to-order manufacturing model, Seagate is enhancing efficiency and ensuring that supply is more closely aligned with customer needs. Combined with disciplined supply strategies and dynamic pricing, this approach is expected to strengthen margins and expand profitability. Management believes these structural changes, supported by a robust product pipeline, position Seagate to generate stronger cash flows and deliver higher earnings in fiscal 2026.

Seagate’s improving profitability has led management to resume share repurchases, a move that reflects its commitment to enhancing capital returns for shareholders. At the same time, the company is reducing debt and fortifying its balance sheet. With expanding profitability and a stronger financial foundation, Seagate is setting the stage for further deleveraging its balance sheet and has improved financial flexibility in the quarters ahead.

Here’s What Seagate’s Valuation indicates

Seagate stock has been on an impressive run this year, yet its valuation still leaves room for investors to step in. Unlike Palantir, which trades at stretched multiples, Seagate remains attractively priced relative to its growth potential.

The company is well-positioned to benefit from the rising demand for mass data storage. However, STX stock trades at a forward price-earnings ratio of just 21.29x. This appears modest given the growth trajectory ahead. Analysts see Seagate’s earnings per share climbing 27.3% in fiscal 2026, followed by another 32.14% jump in 2027, reflecting that the stock is undervalued.

Is Seagate Stock Still a Buy?

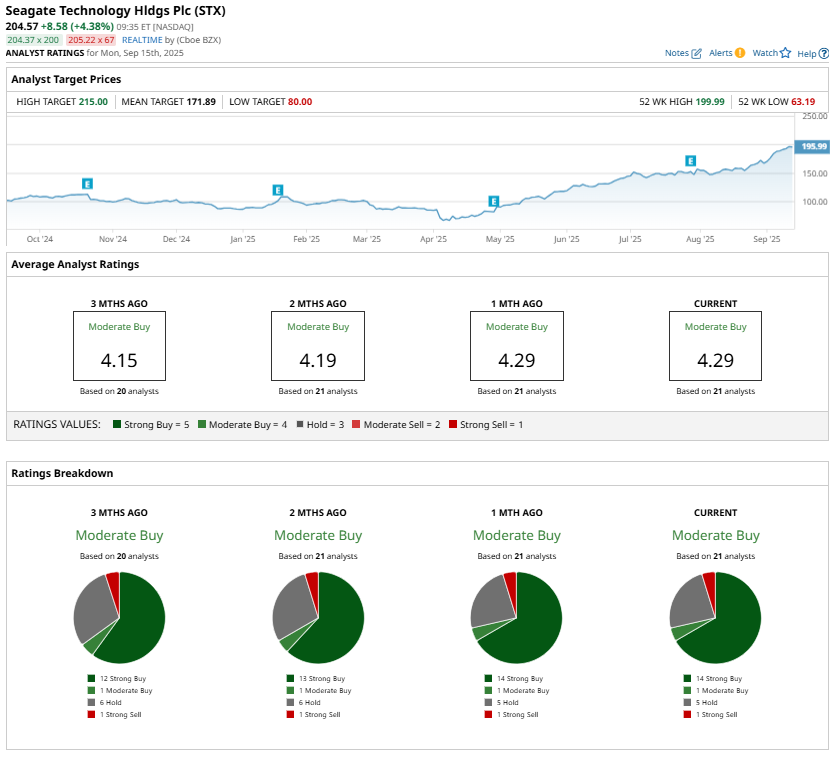

As Seagate stock has appreciated significantly in value, Wall Street has a “Moderate Buy” consensus rating. However, surging demand for its storage solutions led by AI, operational improvements, and a robust product pipeline suggests strong growth ahead.

Furthermore, its low valuation, strong earnings growth projected through 2027, and a commitment to shareholder returns through share repurchases and debt reduction make Seagate a compelling long-term investment with significant upside potential.

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.